If you're still paying vendors by check, you're spending $4-8 per payment on a process that takes 5-7 business days and exposes you to check fraud. ACH (Automated Clearing House) transfers are faster, cheaper, and more secure. But within the ACH system, you have a choice: standard processing or same-day processing. Understanding the difference helps you make smarter payment decisions, especially in hospitality where timing can affect everything from vendor relationships to event execution.

This guide covers how ACH actually works, the real differences between same-day and standard processing, what each costs, and when to use which option.

How ACH Works

Before comparing same-day and standard ACH, it helps to understand the underlying system.

The ACH Network is a batch-processing system operated by Nacha (the National Automated Clearing House Association). Unlike wire transfers, which are processed individually and in real time, ACH transactions are collected into batches and processed at specific intervals throughout the day.

Here's the simplified flow of an ACH payment:

- Origination: Your business (the originator) submits a payment instruction to your bank (the Originating Depository Financial Institution, or ODFI)

- Batching: Your bank collects ACH entries and forwards them to an ACH operator (the Federal Reserve or EPN)

- Processing: The ACH operator sorts the transactions and distributes them to the receiving banks (Receiving Depository Financial Institutions, or RDFIs)

- Settlement: The receiving bank credits the vendor's account and the funds settle between the two banks

The timing of steps 2-4 is where the difference between same-day and standard ACH lives.

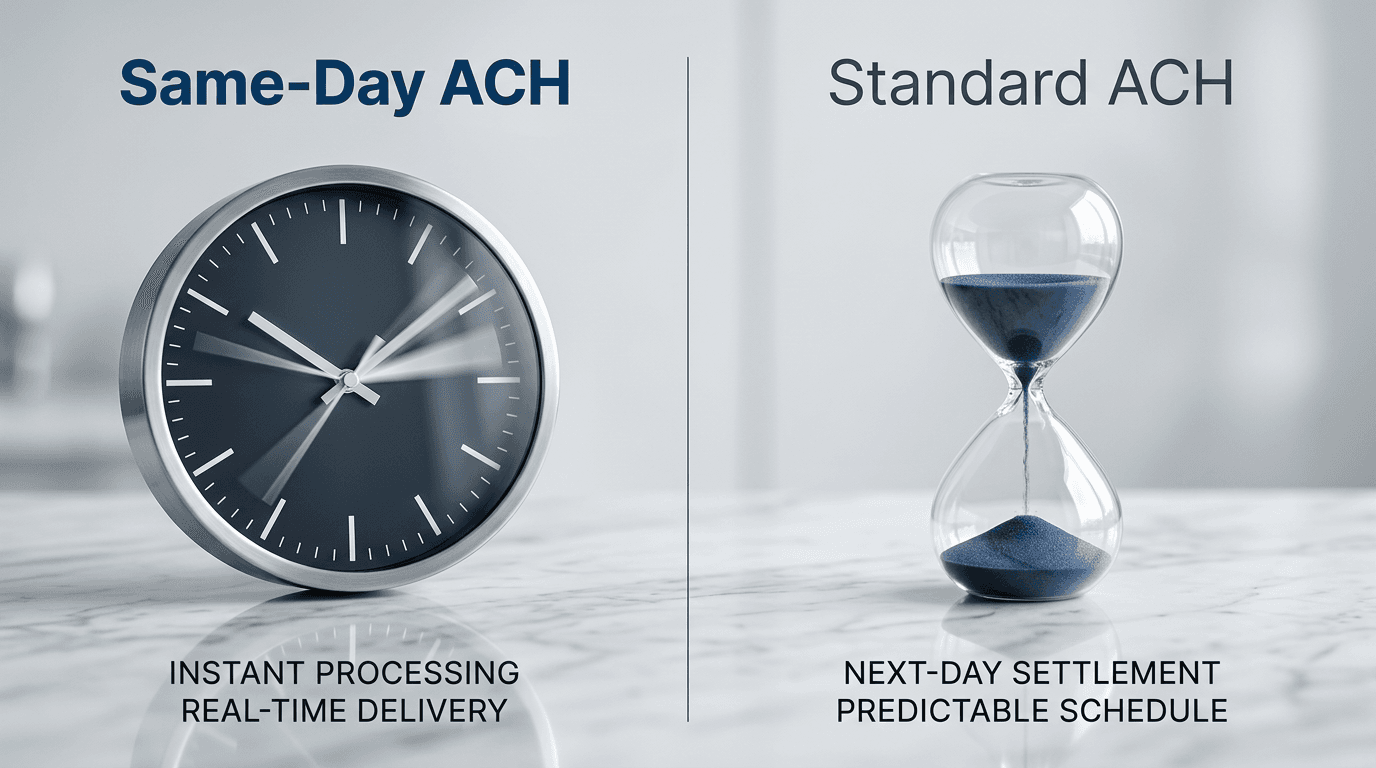

Standard ACH: The Default

Standard ACH is the default processing mode and has been the backbone of business-to-business payments for decades.

Processing Timeline

Standard ACH transactions are processed through the ACH Network in overnight batches. Here's the typical timeline:

- Day 1: You submit the payment before your bank's cutoff time (usually 4:00-5:00 PM ET)

- Day 1 (overnight): Your bank batches the transaction and sends it to the ACH operator

- Day 2: The ACH operator processes and distributes the transaction to the receiving bank

- Day 2-3: The receiving bank posts the credit to the vendor's account

In practice, standard ACH payments are typically available to the recipient 1-2 business days after submission, though some banks post credits on the morning of the second business day.

Important: ACH does not process on weekends or federal holidays. A payment submitted on Friday afternoon won't begin processing until Monday.

Cost

Standard ACH is one of the cheapest electronic payment methods available. Costs vary by bank and platform, but typical ranges are:

- Per-transaction fee: $0.20-$1.00

- Monthly fees: Some banks charge flat monthly fees for ACH services ($10-$50)

- No per-transaction percentage: Unlike credit cards, ACH doesn't charge a percentage of the transaction amount

For hospitality businesses processing hundreds of vendor payments per month, the per-payment cost advantage over checks ($0.50 vs. $4-8) adds up quickly.

Best Use Cases in Hospitality

Standard ACH works well for:

- Regular vendor payments with net-30 or net-15 terms where timing is predictable

- Recurring payments like rent, insurance, and subscription services

- Payroll processing (most payroll is processed via standard ACH)

- Large-volume payment runs where the 1-2 day timeline is acceptable

Same-Day ACH: When Speed Matters

Nacha introduced same-day ACH in 2016, and it has expanded significantly since then. As of March 2026, the per-transaction dollar limit for same-day ACH is $1 million, covering the vast majority of hospitality vendor payments.

Processing Timeline

Same-day ACH uses additional processing windows throughout the day. The current schedule includes three processing windows:

- Window 1: Submissions by 10:30 AM ET, settlement by 1:00 PM ET

- Window 2: Submissions by 2:45 PM ET, settlement by 5:00 PM ET

- Window 3: Submissions by 4:45 PM ET, settlement by 6:00 PM ET (this window supports credits only, which covers outgoing payments)

If you submit a same-day ACH payment at 9:00 AM ET on a Tuesday, your vendor's bank typically receives the funds by 1:00 PM ET that same day. The vendor's bank may make the funds available immediately or by end of day.

Cost

Same-day ACH carries a premium over standard ACH:

- Per-transaction fee: $1.00-$5.00 (varies by bank and platform)

- Nacha fee: Nacha charges the ODFI $0.028 per same-day ACH transaction (this is usually passed through to you)

- Still no percentage-based fee: Even with the premium, same-day ACH is far cheaper than a wire transfer ($15-$35) for the same speed

Best Use Cases in Hospitality

Same-day ACH becomes valuable in specific hospitality scenarios:

- Event vendor payments: A production crew needs to be paid the day after an event. Same-day ACH gets funds to them without the cost of a wire.

- Urgent vendor payments to maintain a critical relationship (your linen service threatens to stop deliveries, and you need to clear a past-due balance today)

- Last-minute contractor payments when a freelancer needs payment before they'll commit to an upcoming gig

- Capturing early-pay discounts when you're close to the discount deadline and standard ACH would miss it

- Settling event-related expenses quickly to close your event P&L faster

Side-by-Side Comparison

Nacha Rules Every Hospitality Business Should Know

The ACH Network operates under Nacha's Operating Rules. Here are the rules most relevant to hospitality businesses making vendor payments.

Authorization Requirements

Every ACH payment requires proper authorization from the originator. For business-to-business payments (SEC code CCD or CTX), this means you need a written agreement with the vendor authorizing ACH payments. This is typically covered in your vendor agreement or during the vendor onboarding process.

Prenotification (Prenote)

Before sending a live ACH payment to a new vendor, you can send a zero-dollar "prenote" transaction to verify the routing and account numbers. The prenote takes 3 business days to process. If the receiving bank rejects it (invalid account number, closed account), you find out before a live payment fails.

Many hospitality businesses skip prenotes to save time, but failed payments create their own delays and vendor relationship problems. A 3-day prenote upfront can save a week of back-and-forth when a payment bounces.

Return Codes

ACH payments can be returned by the receiving bank for various reasons. The most common return codes hospitality businesses encounter:

Returns on standard ACH must be initiated within 2 business days of settlement. For same-day ACH, the return window is also 2 business days but measured from the same-day settlement.

Fraud Monitoring

Nacha requires all participants in the ACH Network to implement risk management practices. For originators (you), this means:

- Verifying vendor identities and bank account ownership before sending payments

- Monitoring for unusual payment patterns (sudden changes in amount, frequency, or destination)

- Maintaining records of all ACH agreements and authorizations

For more on protecting your business from payment fraud, see our payment fraud prevention guide.

Making the Right Choice for Each Payment

The decision between same-day and standard ACH shouldn't be one-size-fits-all. Here's a practical framework for hospitality businesses.

Default to Standard ACH

For the majority of your vendor payments (routine food and beverage deliveries, monthly services, recurring contracts), standard ACH is the right choice. The 1-2 day processing time is more than adequate when you're paying against net-15 or net-30 terms, and the lower cost adds up across hundreds of monthly payments.

Use Same-Day ACH Strategically

Reserve same-day ACH for situations where the speed premium is justified:

- Early-pay discount capture: If paying today earns a 2% discount on a $5,000 invoice, the $3 same-day ACH fee is trivial compared to the $100 you'll save

- Event settlements: Production crews and event vendors expect fast payment. Same-day ACH gets funds there without the cost of a wire.

- Vendor relationship management: When a critical vendor needs immediate payment, same-day ACH demonstrates reliability without the overhead of a wire transfer

- Cash flow timing: When you want to hold cash as long as possible but still meet a payment deadline, same-day ACH gives you maximum flexibility

Avoid Same-Day ACH For

- Routine weekly payment runs where standard timing is adequate

- Very large payments where the dollar limit ($1M) might be a constraint

- Payments where you want maximum time for review and potential recall

Ready to simplify your AP workflow?

Get early access to Cleo Pay and see how we help hospitality teams save hours every week.

How Cleo Pay Handles ACH Payments

Cleo Pay is built for hospitality businesses that need flexible payment options without the complexity of managing multiple payment rails.

Both Options, One Platform

Every payment you process through Cleo Pay can be sent via standard or same-day ACH. You choose the speed at the time of payment based on the specific situation, not based on system limitations. The platform clearly shows the cost and expected delivery time for each option before you confirm.

Vendor Banking Verification

When vendors onboard through Cleo Pay, their banking information is verified through micro-deposit confirmation or instant account verification. This eliminates the most common cause of ACH returns (incorrect routing or account numbers) and means your first payment goes through cleanly.

Payment Scheduling

Schedule payments to maximize your cash flow:

- Schedule in advance: Set a payment to execute on a specific future date using standard ACH

- Just-in-time payments: Use same-day ACH to pay as late as possible while still meeting your obligations

- Recurring schedules: Set up automatic payments for fixed monthly expenses (rent, insurance, SaaS subscriptions)

Real-Time Status Tracking

Track every ACH payment from submission through settlement. Know exactly when your vendor will receive funds, and get notified immediately if a payment is returned. No more calling your bank to check on a payment status or wondering if a vendor received the funds.

Transitioning from Checks to ACH

If your hospitality business is still paying a significant percentage of vendors by check, here's how to make the transition.

Step 1: Identify Check-Heavy Vendors

Pull a report of all vendors you paid by check in the last 90 days. Rank them by payment volume. Focus on the top 20; they probably represent 80% of your check volume.

Step 2: Collect Banking Information

Contact your top vendors and request their ACH payment details (routing number and account number). Many vendors prefer ACH because they get paid faster. Frame it as an upgrade: "We're moving to electronic payments so you'll receive funds 3-5 days faster."

Step 3: Send Prenotes

Before the first live payment, send a prenote to verify the banking information. This takes 3 business days but prevents embarrassing payment failures.

Step 4: Process First ACH Payments

Start with smaller, routine payments while you and your vendors adjust to the new process. Monitor for returns during the first two payment cycles.

Step 5: Expand and Optimize

Once your top vendors are on ACH, work through the rest of your vendor list. For vendors who resist the transition, understand their concerns (some small vendors worry about ACH security or prefer the physical record of a check) and address them directly.

The cost savings alone make this transition worthwhile: $4-8 per check versus $0.25-$1.00 per ACH payment. For a business processing 400 payments per month, switching from 60% checks to 90% ACH saves $10,000-$15,000 annually.

Key Takeaways

- Standard ACH is cheaper ($0.20-$1.00/transaction) and processes in 1-2 business days. Use it for routine vendor payments.

- Same-day ACH costs more ($1.00-$5.00/transaction) but settles the same day. Use it for time-sensitive payments, discount capture, and event settlements.

- Neither processes on weekends or holidays. Plan your payment cycles accordingly.

- ACH is significantly more secure than checks. No physical instruments to intercept, alter, or forge.

- Nacha rules require proper authorization and monitoring. Build these into your vendor onboarding process.

- The transition from checks to ACH pays for itself through reduced per-payment costs, faster processing, and lower fraud risk.

For hospitality businesses ready to modernize their payment operations, Cleo Pay provides both standard and same-day ACH in a platform built specifically for restaurants, hotels, venues, and production companies.